Blockchain technology is one of the most important new technologies today. Many people think blockchain is only used for Bitcoin, but it is also used in many other areas like healthcare, finance, supply chains, and government services. Although blockchain may look difficult at first, it is actually a simple idea that anyone can learn. It is a system that stores information safely and shares it without needing a middle person. This guide helps beginners understand how blockchain works, where it is used in real life, and what its benefits and limits are. Whether you are a student, professional, or just curious, learning about blockchain will help you understand this powerful and growing technology.

What Is Blockchain Technology?

Blockchain is a special technology that helps keep track of transactions in a way that makes it really hard to change past records. Imagine blockchain technology as a shared digital notebook that many people update at the same time. Each page in this notebook, called a "block," contains a list of transactions. Also, these pages are connected in a secure way, forming a chain.

The term "blockchain" describes this process perfectly: it’s a series of blocks of information linked together safely. This ensures that everyone can trust the information in the notebook, since it's nearly impossible to alter what has already been recorded.

Evolution of Blockchain Technology

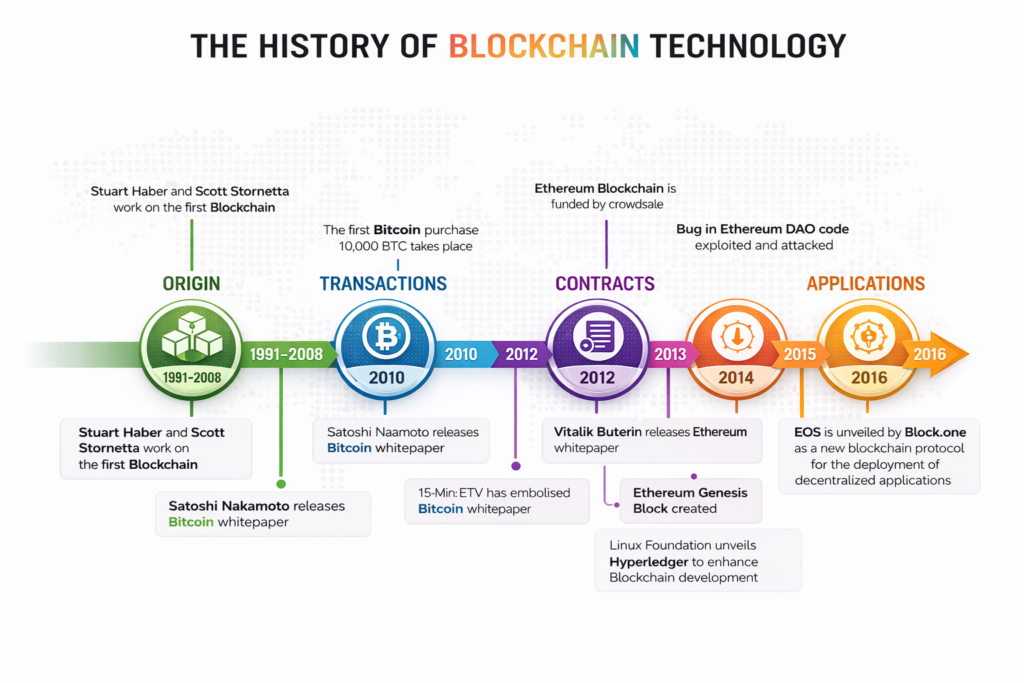

Blockchain technology has changed a lot over time. It started as a way to send digital money and has now become a base technology for apps, finance, and digital governance. Below is a simple, step-by-step explanation.

1. Origins: Basic Ideas Before Blockchain (1970s–2008)

Before blockchain was created, some important ideas already existed:

- Cryptography: Keeps data safe using codes

- Distributed systems: Many computers work together

- Merkle Trees: Help check data quickly

- Byzantine Fault Tolerance: Helps systems work even if some users cheat

These ideas made blockchain possible, but no one had combined them yet.

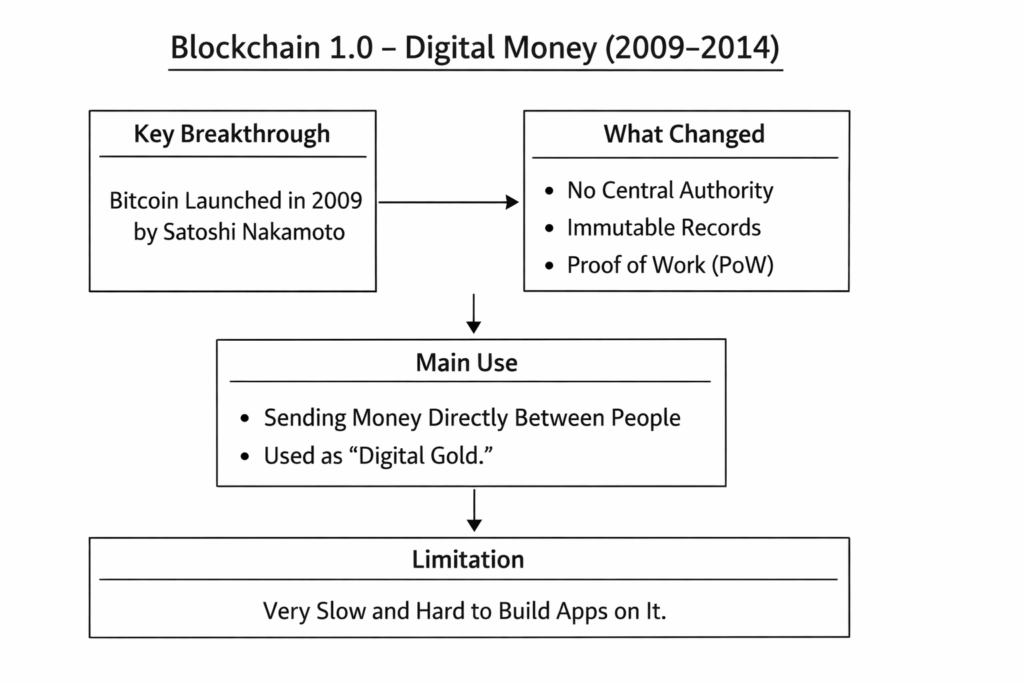

2. Blockchain 1.0 – Digital Money (2009–2014)

Key Breakthrough

- Bitcoin was launched in 2009 by Satoshi Nakamoto.

What Changed

- First system without a central authority

- Records could not be changed

- Used Proof of Work (PoW) to secure the network

Main Use

- Sending money directly between people

- Used as “digital gold.”

Limitation: Very slow and hard to build apps on it.

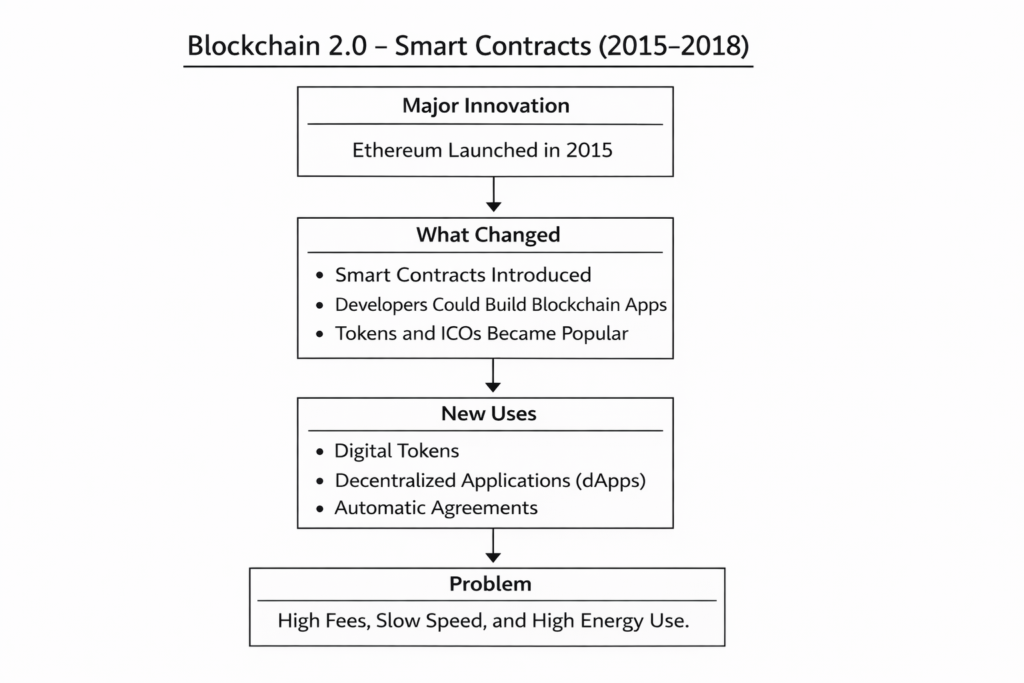

3. Blockchain 2.0 – Smart Contracts (2015–2018)

Major Innovation

- Ethereum was launched in 2015.

What Changed

- Smart contracts were introduced

- Developers could build blockchain apps

- Tokens and ICOs became popular

New Uses

- Digital tokens

- Decentralized applications (dApps)

- Automatic agreements

Problem: High fees, slow speed, and high energy use.

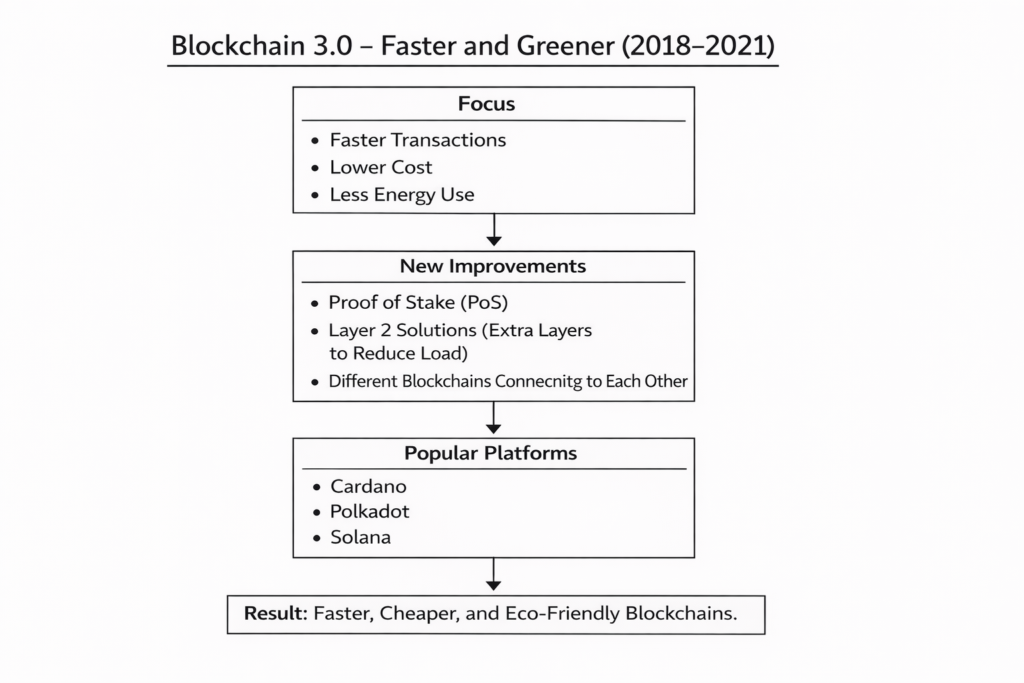

4. Blockchain 3.0 – Faster and Greener (2018–2021)

Focus

- Faster transactions.

- Lower cost.

- Less energy use.

New Improvements

- Proof of Stake (PoS).

- Layer 2 solutions (extra layers to reduce load).

- Different blockchains connecting to each other.

Popular Platforms

- Cardano

- Polkadot

- Solana

Result: Faster, cheaper, and eco-friendly blockchains.

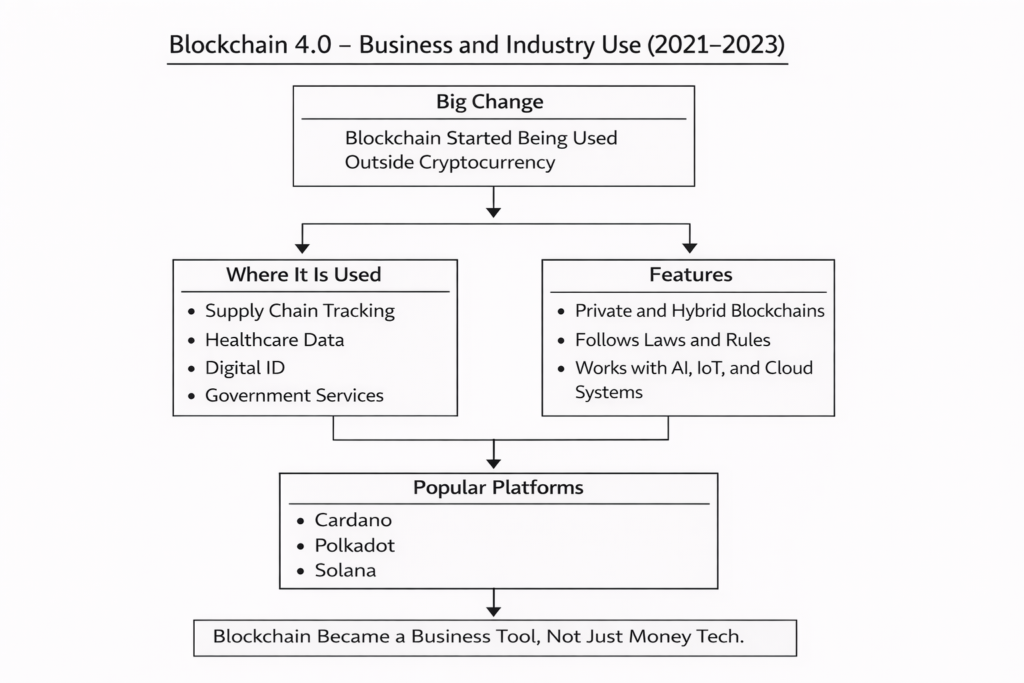

5. Blockchain 4.0 – Business and Industry Use (2021–2023)

- Big Change: Blockchain started being used outside of cryptocurrency.

- Where It Is Used

- Supply chain tracking

- Healthcare data

- Digital ID

- Government services

- Features

- Private and hybrid blockchains

- Follows laws and rules

- Works with AI, IoT, and cloud systems

Blockchain became a business tool, not just money tech.

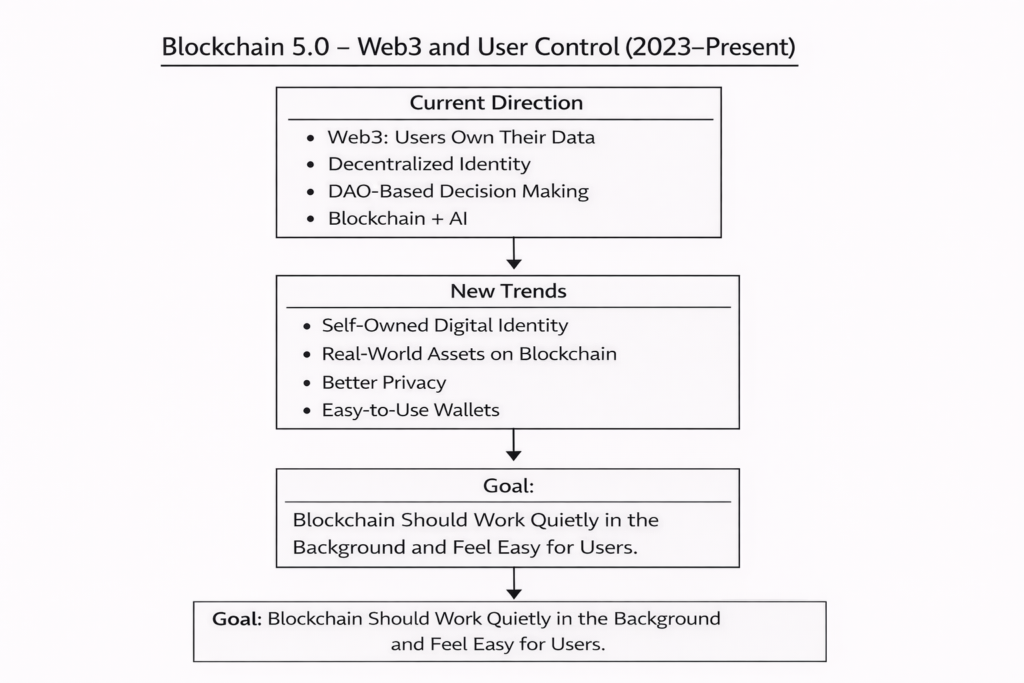

6. Blockchain 5.0 – Web3 and User Control (2023–Present)

Current Direction

- Web3: Users own their data

- Decentralized identity

- DAO-based decision making

- Blockchain + AI

New Trends

- Self-owned digital identity

- Real-world assets on blockchain

- Better privacy

- Easy-to-use wallets

Goal: Blockchain should work quietly in the background and feel easy for users.

Simple Timeline

| Year | Stage | Main Focus |

| 2009 | Blockchain 1.0 | Digital Money |

| 2015 | Blockchain 2.0 | Smart Contracts |

| 2018 | Blockchain 3.0 | Speed & Scalability |

| 2021 | Blockchain 4.0 | Business Use |

| 2023+ | Blockchain 5.0 | Web3 & User Ownership |

Key Characteristics of Blockchain

Blockchain technology has a few key features that set it apart:

- Decentralized: Instead of being controlled by a single organization, like a bank, a blockchain is maintained by a group of computers all over the world. Each of these computers has a complete copy of the entire record, which means there’s no need for middlemen.

- Transparent: Every transaction made on a blockchain is visible to everyone in the network. This openness helps build trust among users, as they can see all activities happening on the blockchain.

- Immutable: Once a transaction is added to the blockchain, it can’t be changed or removed. This is only allowed with the agreement of most participants in the network, making it very difficult to tamper with.

- Secure: Blockchain uses complex coding techniques to keep data safe. Each transaction is protected by sophisticated mathematical methods, which makes it nearly impossible for anyone to hack in.

- Consensus-Based: For a transaction to be approved and recorded, a majority of the network's computers must agree that it's legitimate. This system helps to ensure that any fraudulent activity is quickly identified and rejected.

These features work together to create a reliable and safe way to conduct transactions digitally.

How Blockchain Works: A Step-by-Step Explanation

Understanding how blockchain technology works is essential for grasping its potential and limitations. Here's a detailed breakdown of the process:

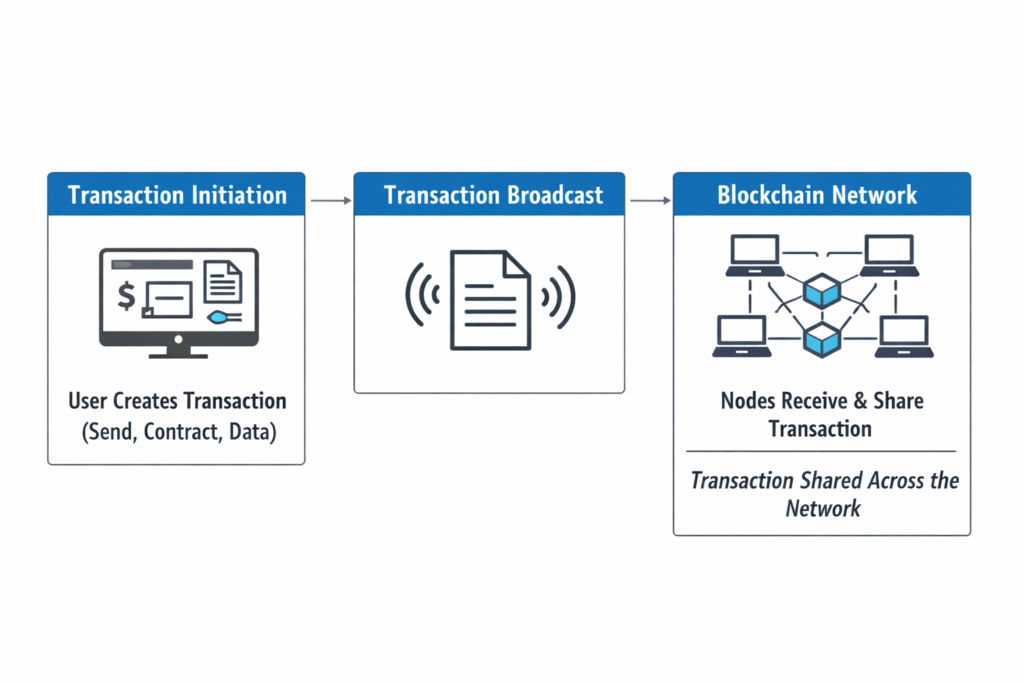

Step 1: Transaction Initiation

When someone wants to make a transaction on the blockchain, they start by inputting the necessary details, like sending money, creating a contract, or exchanging information. Once the transaction is set, it gets shared with all the computers in the network that keep the blockchain running. This way, everyone in the network can see and verify the transaction.

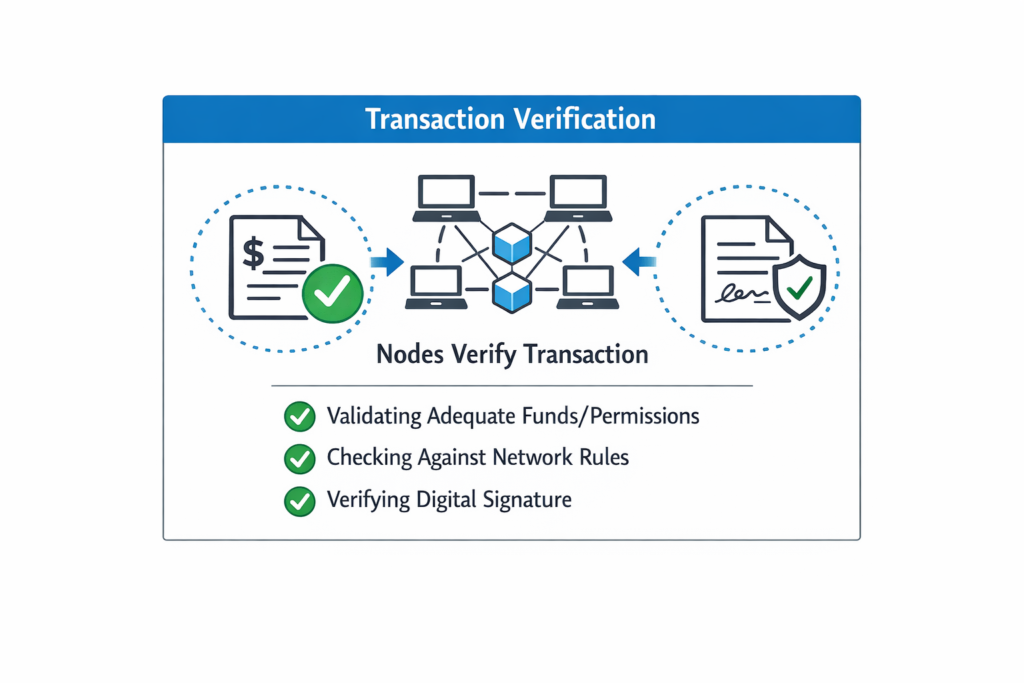

Step 2: Transaction Verification

When a transaction is started, it doesn't go straight onto the blockchain. First, it needs to be checked. Network computers, called nodes, look over the transaction to make sure that:

- The person sending the money has enough funds or permission to do so.

- The transaction meets the network's rules.

- The digital signature is valid, which verifies that the transaction really comes from the right sender.

In blockchain technology, this checking process uses advanced security methods to confirm that each transaction is genuine as well as trustworthy.

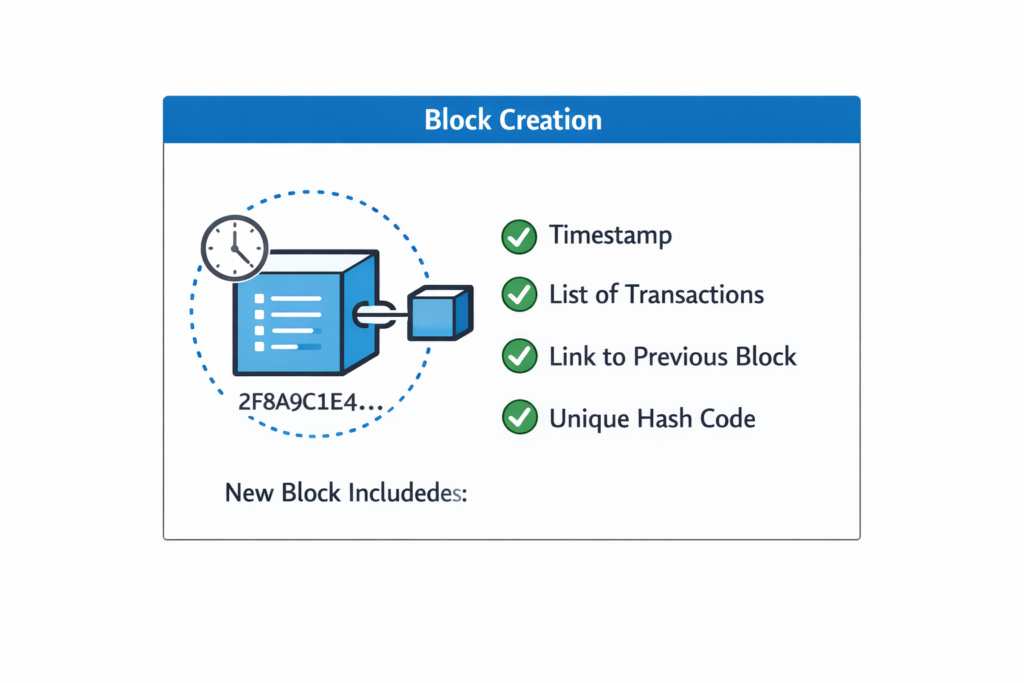

Step 3: Block Creation

When a group of transactions is confirmed as legitimate, they are bundled together to create a new block in a chain. Each block includes:

- A timestamp that shows when it was created

- Information about the transactions it contains

- A link to the previous block, which helps form a continuous chain

- A unique code that identifies this particular block

This unique code is generated using a special formula that takes all the information in the block and turns it into a fixed-length string of letters and numbers. This process ensures that each block is distinct and secure.

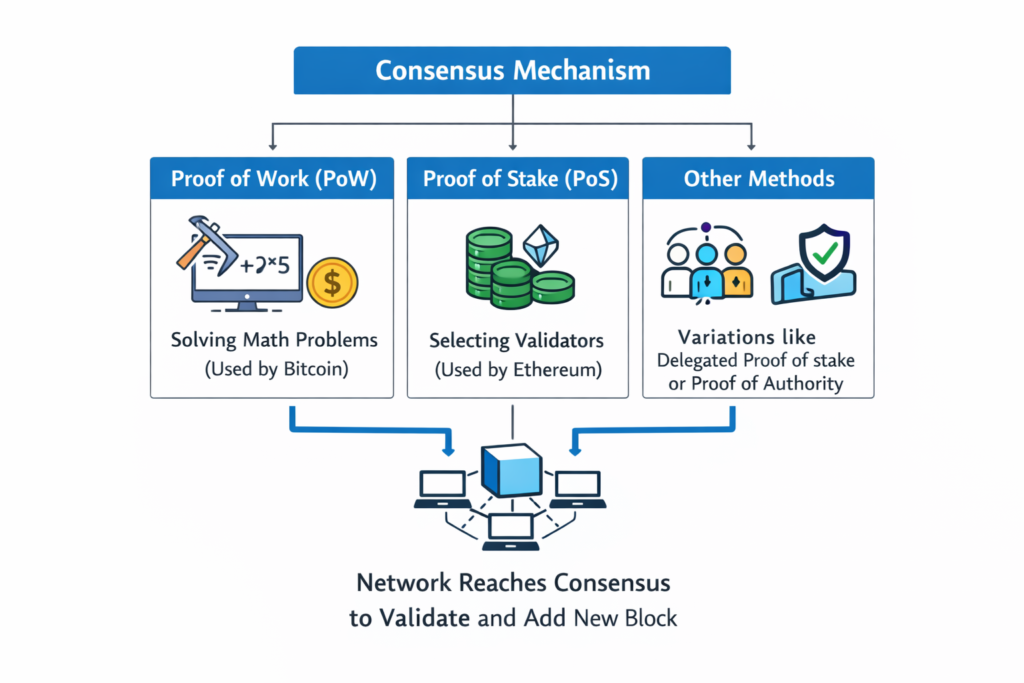

Step 4: Consensus Mechanism

Before a new block of information can be added to a blockchain, the network must come to an agreement that the block is legitimate. Different blockchains use different methods to reach this agreement:

- Proof of Work (PoW): This is the method used by Bitcoin. It requires computers (or "nodes") to solve difficult math problems to confirm transactions. The first computer to solve the problem gets to add the new block to the chain and earns a reward for their efforts.

- Proof of Stake (PoS): This is the method used by Ethereum. Instead of solving math problems. It chooses validators based on how much cryptocurrency they own and are willing to "stake," or set aside, as a guarantee.

- Other Methods: Some blockchain technology use variations of these approaches, like Delegated Proof of Stake or Proof of Authority. Which have their own ways of confirming transactions.

These methods help keep the blockchain secure and ensure that everyone agrees on what information is valid.

Step 5: Block Addition and Distribution

When everyone agrees on a new block of information, that block is added to the end of a blockchain. It's important to note that you can’t insert new blocks in between existing ones or take out blocks without the whole network being aware. Once a new block is added, every computer connected to the network updates its own version of the blockchain to include this new information.

Step 6: Transaction Completion

The transaction is now final and cannot be changed. Every version of the blockchain, which is like a public ledger, has the same information about this transaction. This way of keeping records in many places makes blockchain very secure. In order to change anything, a hacker would have to break into thousands of computers all at once, which is extremely difficult to do.

Understanding Hashing and Cryptography

Hashing plays a key role in keeping blockchain secure. Essentially, when we hash data, we're transforming it into a string of characters of a fixed size using a specific mathematical process. Here's why hashing is so important:

- If you take the same data and hash it, you will always get the same string of characters.

- Even the smallest change in the data results in a completely different hash.

- Once data is hashed, it's nearly impossible to go back and find the original data from the hash.

This means that if someone tries to change the information in a part of the blockchain, the hash would change, signaling that this section is no longer valid. Because each new block in the chain includes a reference to the hash of the previous block, altering one block would mean that all the blocks that come after it would also need to be changed. This is a nearly impossible task to manage on a secure network, making it very hard to tamper with the data.

How to Learn Blockchain Technology: A Beginner's Path

Before getting into blockchain, it's useful to know a few things:

- A basic idea of how cryptography works is about keeping information secure.

- Some familiarity with how databases store information and how different systems can work together.

- Some programming skills can be helpful, especially with languages like Python, Solidity, or JavaScript.

- A general understanding of financial concepts and how transactions work.

That said, you don't need to be an expert in any of these areas to start learning the basics of blockchain.

Learning Resources and Approaches

If you're interested in learning about blockchain technology, there are several great options available:

- Books: There are also some helpful books on the subject. For instance, "Mastering Bitcoin" and "The Basics of Bitcoins and Blockchains" provide a solid understanding of how blockchain works and its importance.

- Developer Communities: Joining online communities can be really beneficial. Websites like GitHub, Stack Exchange, and Discord are filled with people who are also learning about blockchain. You can ask questions, share ideas, and get advice from others.

- Hands-On Practice: One of the best ways to learn is by trying it out yourself. You can start a simple blockchain project or use practice networks to explore how existing blockchains function.

These resources can help you gain a better understanding of blockchain technology in a more accessible way.

Real-World Applications of Blockchain Technology

Financial Services and Banking

The most developed use of blockchain is in the finance sector. Here are a few key ways banks are utilizing it:

- International Transfers: Blockchain allows for quick and low-cost money transfers between countries without the need for multiple banks to process the transaction.

- Automated Agreements: With blockchain, financial contracts can be set up to automatically execute when specific conditions are met, making transactions smoother and error-free.

- Digital Money: Some countries are working on their own digital currencies that are built on blockchain technology.

- Preventing Fraud: The technology creates permanent records of all transactions, which helps banks meet regulations and detect fraudulent activities more effectively.

Overall, blockchain is helping to make financial services faster, more efficient, and more secure.

Supply Chain Management

Blockchain's transparency and traceability make it ideal for supply chain management:

- Product tracking: Every step from manufacturer to consumer is recorded and verifiable

- Counterfeit prevention: Consumers can verify the authenticity of products using blockchain records

- Food safety: In case of contamination, blockchain enables rapid identification of the affected products and their sources

- Sustainability verification: Companies can prove ethical sourcing and production practices

Healthcare

Healthcare organizations are leveraging blockchain for:

- Electronic health records (EHRs): Secure, portable patient records that patients control.

- Pharmaceutical supply chain: Tracking medications to prevent counterfeits. Clinical trials: Transparent, secure patient data management.

- Insurance claims: Automated claims processing through smart contracts.

Government and Public Services

Governments worldwide are exploring blockchain applications:

- Land registry: Immutable records of property ownership reduce disputes and fraud.

- Voting systems: Blockchain-based voting ensures security and transparency.

- Digital identity: Sovereign digital identities that citizens control.

- Licensing and certifications: Tamper-proof records of credentials and qualifications.

Other Emerging Application of Blockchain Technology

- Intellectual Property: NFTs and blockchain-based copyright protection.

- Real Estate: Property transfers and fractional ownership through tokenization.

- Education: Secure, verifiable degree and credential records.

- Energy Trading: Peer-to-peer energy trading and grid management.

What is an Advantage of Using Blockchain Technology?

Better Security and Protection of Information

It uses special security measures that make it extremely difficult for anyone to break in or change the information stored. Because it’s decentralized, there’s no single point that can fail. Even if one part of the system is compromised, many other parts still keep the records safe and correct.

Greater Openness and Trust

All transactions in a blockchain are visible to everyone involved in the network. This openness helps build trust, as people can independently check and confirm transactions. This is especially beneficial in areas where trust issues have existed, like during product shipments or in charitable organizations.

Lower Costs

Blockchain technology cuts down on expenses by removing the need for middlemen like banks or payment services. This means that transaction costs can be drastically lowered, often by 50-90%, depending on the industry.

Faster and More Efficient Processes

In traditional systems, getting approvals often involves multiple steps and can take a long time, sometimes days or weeks. In contrast, blockchain transactions can be completed in just a few minutes or even seconds, and they are available around the clock, no matter where you are in the world.

Permanent Records and Tracking

Once information is added to the blockchain, it can’t be changed. This creates a solid, trustworthy record of everything that has happened, which is important for meeting rules, resolving disputes, and keeping historical records.

Disadvantage of Blockchain Technology

- Scalability Problem: Blockchain systems are slow. They can handle only a few transactions at a time compared to normal payment systems.

- High Energy Use: Some blockchains use a lot of electricity to work. This creates serious environmental problems.

- Unclear Laws and Rules: Blockchain laws are different in every country and keep changing. This makes companies unsure about using it.

- Mistakes Cannot Be Reversed: Once information is added to the blockchain, it cannot be removed. If a mistake happens, it is hard to correct.

- Technical Complexity: Blockchain technology is hard to understand and use. Skilled developers are few and costly.

- Limited Privacy: Blockchain is not fully private. All transactions are visible, and users can sometimes be tracked.

- Interoperability Issues: Different blockchains cannot easily work together. This reduces their usefulness.

- Large Storage Requirement: Blockchain data keeps increasing in size. Storing all this data is difficult for normal users.

In short, blockchain is useful, but it is slow, difficult, uses a lot of energy, and is still developing.

Future Scope of Blockchain Technology

Emerging Trends and Developments

- Layer 2 Solutions: Technologies like Lightning Network for Bitcoin and Polygon for Ethereum help blockchains work faster. They do this by handling transactions outside the main blockchain.

- Interoperability Protocols: Projects such as Polkadot and Cosmos allow different blockchains to talk to each other and share data easily.

- Central Bank Digital Currencies (CBDCs): Many governments are creating digital versions of their national currencies using blockchain technology.

- Enterprise Blockchain: Companies are using private blockchains where only selected people can access the system. These are also used for business and industry work.

- Integration with IoT and AI: Blockchain is being combined with Internet of Things (IoT) devices and Artificial Intelligence. This generally helps to create systems that can work automatically without human control.

Predicted Market Growth

The global blockchain market was worth about $17.5 billion in 2025. In fact, it is expected to grow very fast, at more than 60% per year, until 2030. This growth is happening because:

- More companies and governments are using blockchain

- New technology is solving old problems

- More industries understand the benefits of blockchain

- Governments are making clearer rules for blockchain use

Challenges to Overcome

Despite promising trends, blockchain must overcome significant hurdles:

- Achieving true scalability without sacrificing security

- Developing sustainable, energy-efficient consensus mechanisms

- Establishing consistent regulatory frameworks globally

- Improving user experience and reducing technical barriers

- Building enterprise-grade security standards

Conclusion

Blockchain technology is a new way to store and share information safely. It was first created for Bitcoin, but now it is used in many industries. Blockchain is not only about cryptocurrency; it helps create systems where trust is shared, data is open to everyone, and middlemen are not needed. Although blockchain has some problems like slow speed, high energy use, and unclear rules, new ideas and technologies are improving it.

In the future, blockchain will grow by becoming faster, easier to use, and better connected with current systems. As this technology develops, people who understand blockchain will have more chances to succeed and make better decisions. Whether you are a student, worker, investor, or just curious, this is a good time to learn about blockchain and how it can be useful in your life and work.